For Brokers

Estimate your max LTV in seconds

Pick the town, product, credit score, and how close the property is — we'll show the maximum loan-to-value we can consider. No sign-up, no obligation.

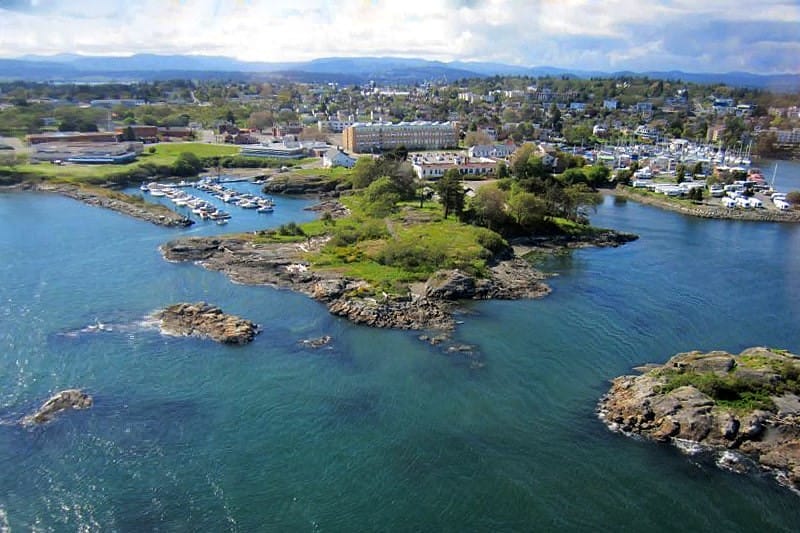

Esquimalt

Lending guidelines for Esquimalt, British Columbia

Last reviewed by Tekamar Mortgage Fund on

Show on MapLending Snapshot

Here’s the deal on Esquimalt: we’ll lend up to 70.0% LTV in this stable, highly dense peninsula market right next to Victoria. The local economy is anchored by CFB Esquimalt, meaning massive federal government employment that keeps the property market incredibly steady. Since it's a dense, mature area, expect to bring us mostly condos, townhomes, and duplexes.

Lending in Esquimalt

Esquimalt is not Victoria, and the locals will be the first to correct you if you mix them up. It is a compact peninsula just a few minutes west of downtown Victoria, but it has a completely different feel. The town is dominated by CFB Esquimalt, home to Canada’s Pacific naval fleet. The base is the primary economic driver here, shaping both local demographics and neighborhood culture. For brokers putting together deals on Vancouver Island, Esquimalt represents a rare pocket of steady, insulated value. For us at Tekamar, it is exactly the kind of predictable market we look for outside the Lower Mainland.

You won’t find suburban sprawl here because there is simply nowhere left to build. Bounded by water on three sides—the Strait of Juan de Fuca, Esquimalt Harbour, and the Gorge waterway—the land supply is physically capped. Growth only happens when someone knocks something down to build upward. Right now, about half of the housing stock consists of low-rise apartments, sitting alongside duplexes and mid-century bungalows. Esquimalt used to be seen as the blue-collar, unpretentious alternative to upscale neighbors like Oak Bay. Today, that secret is out. Young professionals and military families are moving in for the walkable streets and prices that actually make sense compared to the rest of Greater Victoria.

For underwriters, the economic fundamentals are exceptionally stable. This isn’t a seasonal tourism town that shuts down in November. Over 20% of the local workforce is employed directly in public administration. With the naval base and shipyard trades driving employment alongside provincial workers making the short commute into Victoria, your borrowers have highly reliable incomes. It is also an area with massive rental demand, which keeps property values steady and attracts plenty of residential investors.

We often joke that Tekamar is the MIC for towns without stoplights, but we aggressively target strong, urban-adjacent pockets like this. Because geography caps the housing supply, properties here move fast. When we underwrite a file, we always look at the worst-case scenario. If we ever have to take a property back in Esquimalt, we know it won’t sit on the market collecting dust while interest piles up. That predictable exit strategy is why the township scores a perfect 10 out of 10 on our internal desirability index, which lets us offer our maximum loan to value of 70% in this community.

We source our capital from friends and family, so keeping their principal safe dictates every decision we make. But when the underlying real estate is this reliable, we have the confidence to step in where conventional lenders walk away. Whether your client needs a second mortgage to update a 1960s bungalow, a bridge loan to secure a waterfront condo, or an equity-based debt consolidation to clean up their credit, we have funds ready to deploy. Give us the full picture, explain the borrower’s exit strategy, and if the equity makes sense, we will help you get the deal closed.

Local Hospital

Frequently Asked Questions

We cap out at 70.0% LTV in Esquimalt. While the connection to Victoria and the navy base provide great stability, the flat population growth since 2016 and a 7.9% unemployment rate keep us from going higher.

Over 20% of the workforce is in public administration at the CFB Esquimalt navy base and another 13.5% is in healthcare. This heavy government payroll creates a rock-solid economic floor that makes underwriting local buyers a breeze.

Trying to pitch an unusual, non-conforming property with no local comps won't fly. Esquimalt is a dense, urban market, so we want standard condos, duplexes, townhomes, or traditional detached homes that are easy to value.

Our Mortgage Products Available in Esquimalt

| Mortgage Product Name | Max LTV | Key Notes for Esquimalt |

|---|---|---|

| Credit Repair and Debt Consolidation | 70.0% | Standard product terms |

| Variable Income | 70.0% | Standard product terms |

| Bare Land and Unique Properties | 65.0% | Standard product terms |

| Bridge Financing | 70.0% | Standard product terms |

| Equity Lending / Refinance | 70.0% | Standard product terms |

| Purchases | 70.0% | Standard product terms |

Detailed Mortgage Product Information

Credit Repair and Debt Consolidation

Maximum Loan-to-Value (LTV) for Credit Repair and Debt Consolidation in Esquimalt:

70.0 %

“Their credit report reads like a horror novel, but the house was just renovated and is worth a lot…”

Here’s what happens when life takes a wrong turn. A bad business venture. Workplace Injury. That divorce that dragged on for two years. Suddenly your credit score looks like a batting average and the banks won’t even return your calls.

But here’s the thing – none of that changes what your ho...

Variable Income

Maximum Loan-to-Value (LTV) for Variable Income in Esquimalt:

70.0 %

“Their income is all over the map, but there’s definitely income…”

Here’s a funny thing about lending based on Line 15000 of your Notice of Assessment: It’s a neat little box to underwrite against. Works great if you’re a salaried employee. Not so great if you’re running a fishing charter in Campbell River where thres fishing season, and the rest of the year.

We get it. Income isn’t always ti...

Bare Land and Unique Properties

Maximum Loan-to-Value (LTV) for Bare Land and Unique Properties in Esquimalt:

65.0 %

“The appraisal came back as ‘property type: other’…”

Here’s a truth about real estate that nobody wants to admit: not everything fits in a box. Banks have boxes. Nice, tidy boxes labeled “single family home” and “condo” and “townhouse.” Their computer systems literally don’t have a dropdown menu option for “converted church with commercial kitchen” or “geodesic dome on 40 acres.”

We’ve funded...

Bridge Financing

Maximum Loan-to-Value (LTV) for Bridge Financing in Esquimalt:

70.0 %

“Subjects came off their current home last week but their new place closes Friday…”

Here’s a funny thing about bridge financing: everyone thinks it’s complicated. It’s not. Someone needs to close on their new house before their old house sells. Or their sale fell through after they removed subjects on their dream home. Or they found the perfect downsizer condo but haven’t listed the family hom...

Equity Lending / Refinance

Maximum Loan-to-Value (LTV) for Equity Lending / Refinance in Esquimalt:

70.0 %

“They have tons of equity but don’t qualify under B20…”

Here’s the thing about equity lending: it exists because banks literally can’t do it. B20 guidelines require income verification. Full stop. No wiggle room. No common sense exceptions.

We’re provincially regulated. The funds we lend on come from individual investors, not the Bank of Canada. So when your client has 50% equity but their in...

Purchases

Maximum Loan-to-Value (LTV) for Purchases in Esquimalt:

70.0 %

Moving is supposed to be exciting. New town, new job, new chapter. So why do banks act like you’re asking for their firstborn when you need a mortgage?

“You haven’t been at your new job for thre months”

“Your self-employment income doesn’t count in a new market.”

“We need to see established a year if you are part time contract - even if you’re working 40 hours under your new role”

Meanwhile...