Gold River

Lending guidelines for Gold River, British Columbia

Last reviewed by Tekamar Mortgage Fund on

Show on MapLending Snapshot

Gold River is a quiet, post-industrial wilderness town on Vancouver Island where we cap our LTV at 50.0%. The local economy is highly volatile and heavily reliant on forestry and fishing, which makes the buyer pool incredibly thin. Because a forced sale here can take up to nine months, we need a massive equity cushion and a bulletproof borrower story.

Lending in Gold River: What Brokers Need to Know

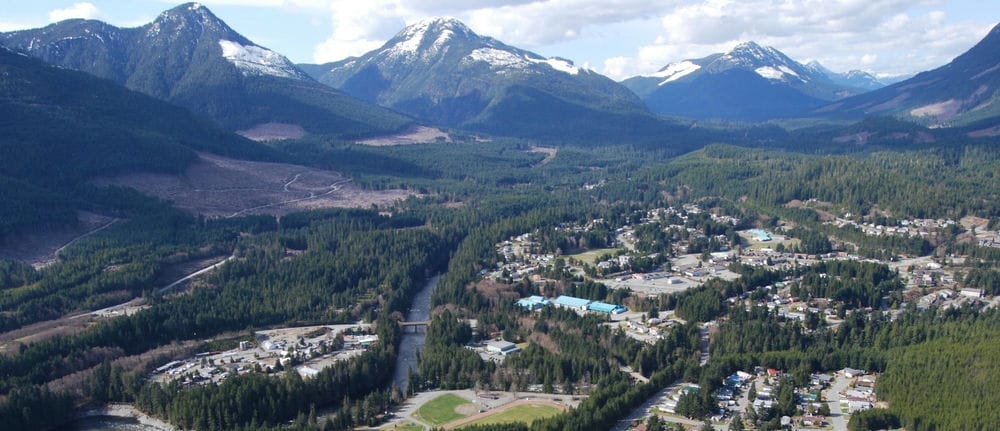

Gold River sits about 90 kilometers west of Campbell River, right at the end of Highway 28. It is a classic Vancouver Island resource town that had to find a second life when the local pulp mill shut down in the late 1990s. Today, it serves as the main drive-in gateway to Nootka Sound. At Tekamar, we focus on lending outside Greater Vancouver and the Fraser Valley, which means we spend a lot of time analyzing remote markets like this. We absolutely write mortgages in Gold River, but we look at these deals with a realistic view of the local economy.

With a population of 1,246 and a median age of 56, the town leans heavily toward retirees and seasonal workers. Seniors aged 65 and older make up 30% of the community. The employment rate sits at 46.3%, with an unemployment rate of 6.5%. While those numbers are stable, the job market is highly concentrated. Forestry, agriculture, and fishing account for exactly 25.0% of all local employment. The rest of the workforce is mostly distributed between healthcare, education, and construction. We score the local economy a 5 out of 10. It is a stable environment for now, but a downturn in the forestry sector or a weak summer tourist season impacts this entire community immediately.

Unlike historic coastal towns that grew organically, Gold River was planned and built from scratch in the 1960s. It was designed as Canada’s first all-electric town with underground wiring. Because of this planning, the municipal infrastructure is in much better shape than you would typically expect for a community of this size. Single-detached houses make up 68.9% of the housing stock, with row houses making up another 16.4%. Most of these properties were built between the 1960s and 1980s. The main draw for buyers here is affordability. Real estate is significantly cheaper than in Campbell River or the Comox Valley. This price point attracts outdoor enthusiasts who want a quiet base of operations and do not mind driving an hour to reach a major hospital or big-box retail.

When we underwrite mortgages in Gold River, our priority is managing illiquidity risk. The town scores a 7 out of 10 for community desirability—people who move here are highly committed to the lifestyle. However, because Gold River is located at the end of a single highway, properties can sit on the market for months if demand softens. If a loan goes into default, the foreclosure process takes longer and carrying costs accumulate quickly. To offset this geographic risk, we cap our maximum loan-to-value ratio in Gold River at 50.0%.

We regularly fund equity take-outs, debt consolidations, and second mortgages in the area. If you have a client purchasing a home, a local contractor looking to pull equity for business cash flow, or a self-employed borrower who needs a clean bridge loan, we can make it work. Just keep that 50.0% LTV limit in mind when structuring the deal.

the Nearest Tim Hortons

the Nearest Costco

Nearest Hospital

Frequently Asked Questions

The buyer pool here is incredibly shallow, meaning a forced sale could take six to nine months and require a 15-25% price discount. We need that 50.0% LTV cap to protect against a slow and costly exit.

With 25% of the economy tied to volatile resources like forestry and fishing, local incomes are risky. To get a deal done, your borrower needs a strong income source that is completely independent of the local economy.

We will pass on any deal where the borrower doesn't have a 50% down payment, lacks a clear and logical reason for moving to this remote town, or relies entirely on local employment.

Our Mortgage Products Available in Gold River

| Mortgage Product Name | Max LTV | Key Notes for Gold River |

|---|---|---|

| Variable Income | 50.0% | Standard product terms |

| Bare Land and Unique Properties | 50.0% | Standard product terms |

| Bridge Financing | 50.0% | Standard product terms |

| Equity Lending / Refinance | 50.0% | Standard product terms |

| Purchases | 50.0% | Standard product terms |

Detailed Mortgage Product Information

Variable Income

Maximum Loan-to-Value (LTV) for Variable Income in Gold River:

50.0 %

“Their income is all over the map, but there’s definitely income…”

Here’s a funny thing about lending based on Line 15000 of your Notice of Assessment: It’s a neat little box to underwrite against. Works great if you’re a salaried employee. Not so great if you’re running a fishing charter in Campbell River where thres fishing season, and the rest of the year.

We get it. Income isn’t always ti...

Bare Land and Unique Properties

Maximum Loan-to-Value (LTV) for Bare Land and Unique Properties in Gold River:

50.0 %

“The appraisal came back as ‘property type: other’…”

Here’s a truth about real estate that nobody wants to admit: not everything fits in a box. Banks have boxes. Nice, tidy boxes labeled “single family home” and “condo” and “townhouse.” Their computer systems literally don’t have a dropdown menu option for “converted church with commercial kitchen” or “geodesic dome on 40 acres.”

We’ve funded...

Bridge Financing

Maximum Loan-to-Value (LTV) for Bridge Financing in Gold River:

50.0 %

“Subjects came off their current home last week but their new place closes Friday…”

Here’s a funny thing about bridge financing: everyone thinks it’s complicated. It’s not. Someone needs to close on their new house before their old house sells. Or their sale fell through after they removed subjects on their dream home. Or they found the perfect downsizer condo but haven’t listed the family hom...

Equity Lending / Refinance

Maximum Loan-to-Value (LTV) for Equity Lending / Refinance in Gold River:

50.0 %

“They have tons of equity but don’t qualify under B20…”

Here’s the thing about equity lending: it exists because banks literally can’t do it. B20 guidelines require income verification. Full stop. No wiggle room. No common sense exceptions.

We’re provincially regulated. The funds we lend on come from individual investors, not the Bank of Canada. So when your client has 50% equity but their in...

Purchases

Maximum Loan-to-Value (LTV) for Purchases in Gold River:

50.0 %

Moving is supposed to be exciting. New town, new job, new chapter. So why do banks act like you’re asking for their firstborn when you need a mortgage?

“You haven’t been at your new job for thre months”

“Your self-employment income doesn’t count in a new market.”

“We need to see established a year if you are part time contract - even if you’re working 40 hours under your new role”

Meanwhile...