Kimberley

Lending guidelines for Kimberley, British Columbia

Last reviewed by Tekamar Mortgage Fund on

Show on MapLending Snapshot

Kimberley is a solid small resort town that successfully pivoted from mining to lifestyle and tourism. Tekamar caps LTV here at 65.0% because the local economy relies heavily on retirees and seasonal tourism rather than high-paying, year-round industries. It’s a stable market, but best suited for buyers with strong outside income or solid equity.

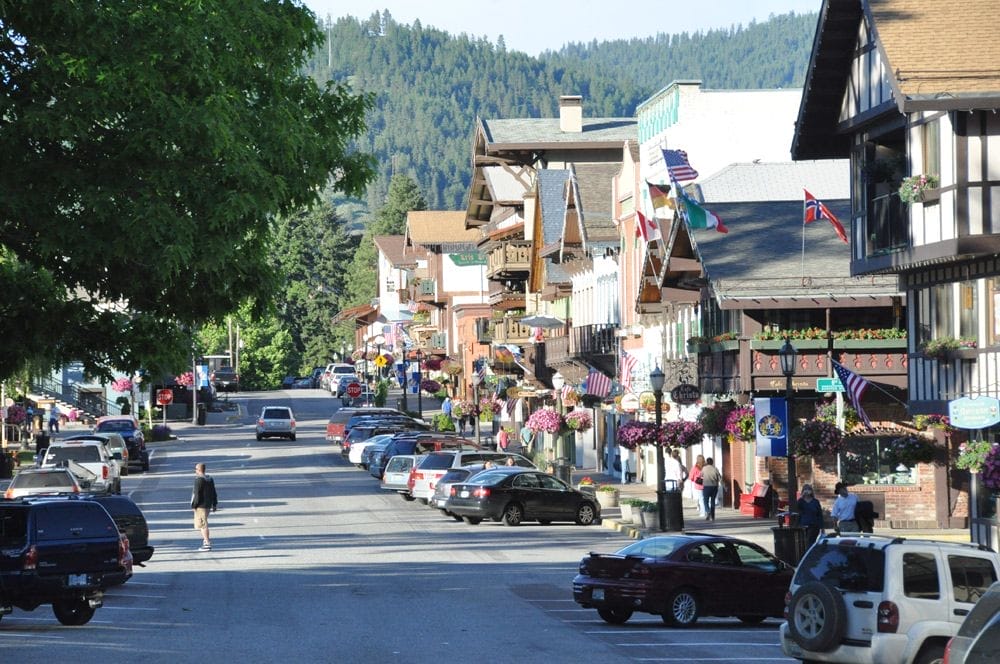

Kimberley: From mining town to resort community

To get a handle on Kimberley’s real estate, you have to look at how this East Kootenay town survived. Located about half an hour up the road from Cranbrook, Kimberley spent decades as a traditional mining town built entirely around the Sullivan Mine. When the mine closed, the city didn’t dry up. Instead, they pulled off a massive pivot, turning the downtown into a Bavarian-themed pedestrian area called the Platzl and rebranding the region as a year-round mountain resort. Today, the population sits at just over 8,100, showing a steady growth of over 9% since 2016. It is exactly the kind of quiet, stable market we look for.

Who is buying here?

This isn’t a temporary work camp or a place where people just pass through. It’s a highly residential community where single-family homes make up more than 76% of the market. The housing stock is a diverse mix: you have old miner cabins and heritage homes downtown, sitting alongside newer, recreation-oriented properties up near the ski resort.

Most of the buyers here are moving for the lifestyle. With a median age of 45, we see a steady flow of retirees, remote workers, and downsizers selling off properties in Vancouver or the Okanagan. They want the ski-in access and mountain trails without the Whistler price tag. Over two-thirds of the local population holds a post-secondary credential, reflecting a highly educated, stable demographic. For us, that consistent demand means properties keep their value and stay liquid, even when interest rates fluctuate.

The local economy

From an underwriting perspective, Kimberley is resilient because it isn’t a one-industry town anymore. Tourism and skiing bring in visitors, but the day-to-day economy is anchored by stable sectors. Healthcare and social assistance lead the way at over 13% of local employment, followed closely by retail trade and accommodation services. Median household incomes are solid, hovering around $81,000.

Kimberley also gets a major boost from its proximity to Cranbrook. More than 40% of working residents enjoy a commute of under 15 minutes, but those who need to travel further can easily head down Highway 95A. This connection to a larger regional hub and airport provides an economic floor for local home values, ensuring the market doesn’t suffer from the volatility typical of isolated mountain towns.

Underwriting in Kimberley

For brokers, Kimberley is a consistent source of alternative deals. We regularly see older homeowners looking to consolidate debt on heritage properties, investors who don’t fit traditional bank guidelines, or buyers who need a quick bridge loan to secure a ski chalet while their primary residence sells.

Because we lend private capital from friends and family, protecting that principal is our first priority. We look closely at average days on market and local liquidity to plan for worst-case scenarios. But because Kimberley’s underlying fundamentals are so strong, we are highly comfortable lending here. We offer up to 65% LTV on qualified files in this community.

If you have a file in the East Kootenays, send it our way. We don’t require perfect credit—just a logical exit plan and solid equity. We know the local drivers and we will give you a straight answer quickly.

the Nearest Tim Hortons

the Nearest Costco

Nearest Hospital

Frequently Asked Questions

We cap lending at 65.0% LTV. While the town has stable lifestyle appeal, it remains a smaller, tourism-dependent market with higher unemployment and less economic depth than a major hub.

With a 7.7% unemployment rate and heavy reliance on pensions and tourism, local wages are modest. Deals go much smoother if your borrower has stable, non-local income or a strong equity position.

Trying to push a high-LTV file with a buyer who relies solely on local resort-industry income will likely sink the deal. Stick to single-family homes, as they make up over 76% of the local housing stock.

Our Mortgage Products Available in Kimberley

| Mortgage Product Name | Max LTV | Key Notes for Kimberley |

|---|---|---|

| Credit Repair and Debt Consolidation | 65.0% | Standard product terms |

| Variable Income | 65.0% | Standard product terms |

| Bridge Financing | 65.0% | Standard product terms |

| Equity Lending / Refinance | 65.0% | Standard product terms |

| Purchases | 65.0% | Standard product terms |

Detailed Mortgage Product Information

Credit Repair and Debt Consolidation

Maximum Loan-to-Value (LTV) for Credit Repair and Debt Consolidation in Kimberley:

65.0 %

“Their credit report reads like a horror novel, but the house was just renovated and is worth a lot…”

Here’s what happens when life takes a wrong turn. A bad business venture. Workplace Injury. That divorce that dragged on for two years. Suddenly your credit score looks like a batting average and the banks won’t even return your calls.

But here’s the thing – none of that changes what your ho...

Variable Income

Maximum Loan-to-Value (LTV) for Variable Income in Kimberley:

65.0 %

“Their income is all over the map, but there’s definitely income…”

Here’s a funny thing about lending based on Line 15000 of your Notice of Assessment: It’s a neat little box to underwrite against. Works great if you’re a salaried employee. Not so great if you’re running a fishing charter in Campbell River where thres fishing season, and the rest of the year.

We get it. Income isn’t always ti...

Bridge Financing

Maximum Loan-to-Value (LTV) for Bridge Financing in Kimberley:

65.0 %

“Subjects came off their current home last week but their new place closes Friday…”

Here’s a funny thing about bridge financing: everyone thinks it’s complicated. It’s not. Someone needs to close on their new house before their old house sells. Or their sale fell through after they removed subjects on their dream home. Or they found the perfect downsizer condo but haven’t listed the family hom...

Equity Lending / Refinance

Maximum Loan-to-Value (LTV) for Equity Lending / Refinance in Kimberley:

65.0 %

“They have tons of equity but don’t qualify under B20…”

Here’s the thing about equity lending: it exists because banks literally can’t do it. B20 guidelines require income verification. Full stop. No wiggle room. No common sense exceptions.

We’re provincially regulated. The funds we lend on come from individual investors, not the Bank of Canada. So when your client has 50% equity but their in...

Purchases

Maximum Loan-to-Value (LTV) for Purchases in Kimberley:

65.0 %

Moving is supposed to be exciting. New town, new job, new chapter. So why do banks act like you’re asking for their firstborn when you need a mortgage?

“You haven’t been at your new job for thre months”

“Your self-employment income doesn’t count in a new market.”

“We need to see established a year if you are part time contract - even if you’re working 40 hours under your new role”

Meanwhile...